Recently, the two most prominent topics in business media were interest rates and inflation — that is, until the prospect of widespread bank failures emerged. Many observers believe that all will contribute to an on-coming (or are driving a currently emerging) recession. If that is true, the question is: a recession of what depth and duration? We don’t pretend to know, but you might ask: Will it affect my surety’s support of my business plan? Not necessarily, although you and your surety broker may have to work at it to make sure.

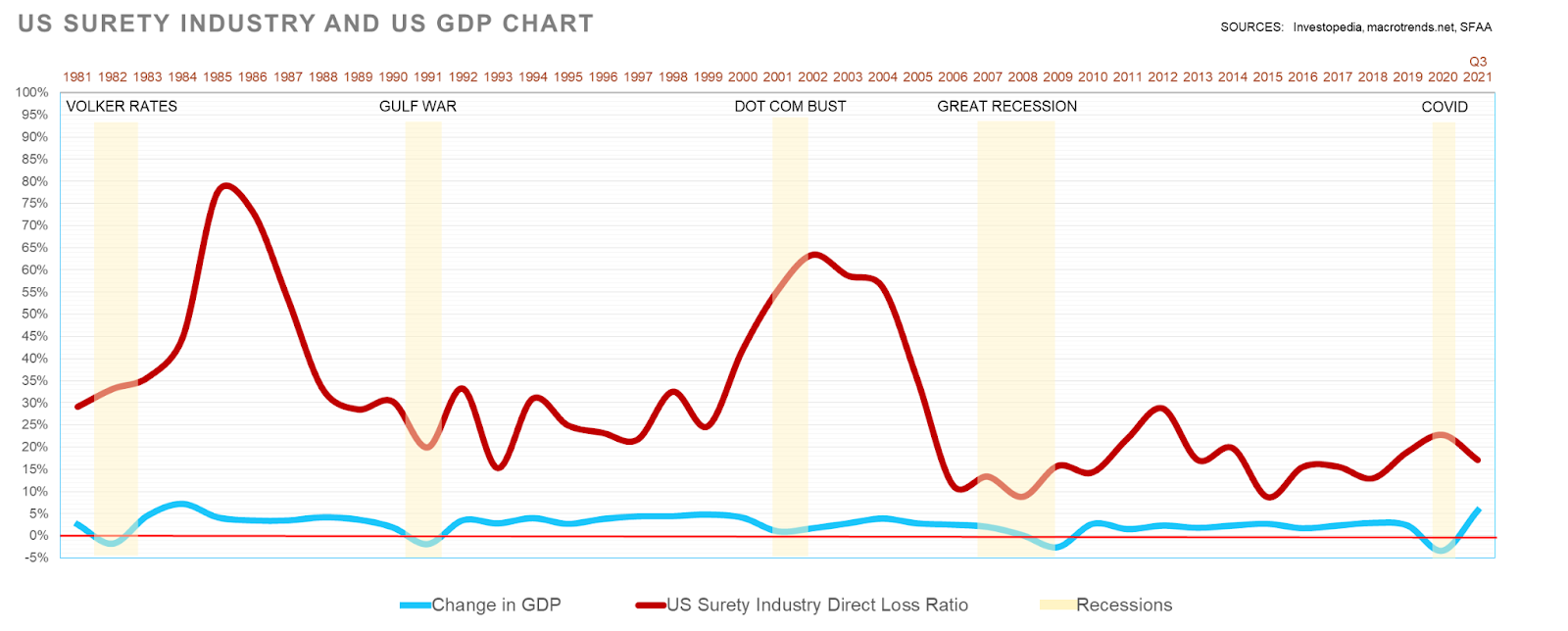

A quick look at the history of surety industry loss cycles offers context for how sureties tend to anticipate and react to recessionary conditions.

The above represents only losses incurred by sureties. It does not reflect the overhead and operating expenses that are also part of a surety’s P&L. Surety Loss Cycles have their own character – Frequency (1991-’92 and 2010-’12), Severity (2001-’03), or both (1983-’86). The timeline above reflects that surety loss cycles tend to commence late in recessions (or even early in the recovery) and accelerate as the economy recovers. Underwriters know this and can be expected to tighten underwriting standards with a recession on the horizon.

A surety’s framework for underwriting even the best-in-class contractor risks are the conditions faced by its total portfolio of clients. To avoid being penalized for the sins of others, contractors need to differentiate their credit profiles. Doing so, will allow them to maintain the surety terms, pricing, and support that provides a competitive advantage when it’s needed the most. Your surety broker is a linchpin in this process. How are you evaluating the performance of your broker in achieving this for your firm? Are they an experienced surety expert or a risk management generalist?

In challenging economic times, the surety industry’s underwriting attention drifts toward the portfolio’s lowest common denominators (i.e. highest risk elements). Assure yourself that your broker is using all the tools at its disposal to separate you from the pack. This involves more than the broker reminding you what a long relationship they’ve had with you and their great relationship with your surety. Relationships are indeed fundamental and critical to surety support, but are not always enough to overcome underwriting decisions based on an incomplete narrative and the absence of data your bonding company never sees.

Contractors should expect increased scrutiny on G&A and estimated margins. Communication is key. Experienced surety underwriters can deal with bad news, but are less accommodating of surprises. Tell your surety where you will cut, if your company is faced with declining volume. And, if you won’t have to, why?

Be transparent and candid on pipeline probabilities for new work and if newly acquired work will involve lower gross margins. What competitive advantages do you have for a particular project? How will you maintain margin discipline in your pricing as competition increases? How are you refining your prequalification of subcontractors? If you are a specialty firm, how do you pick the best GC and CM’s, in your market, to work for?

A prolonged recession will accelerate a buyers’ market for construction services. Underwriters will closely examine the risk transfer owners will seek to achieve through contract language. Find out what your underwriter will or will not accept as bondable contract provisions (expressed or implied warranties, LD’s vs. actual damages, etc.). Your firm’s knowledge and/or prior experience with the owner can be of great value here.

Schedule compression can happen on projects where the asset being built is time-sensitive for beginning to generate a return for the owner or if the public requires use of the finished project. Is the proposed schedule realistic, given the availability of skilled labor and/or material deliveries as you plan to mobilize the job? What technology will be used on projects to promote safety, productivity, identify problems, and avoid delays?

Many aspects of a contractor’s business have already been impacted by inflation, but some additional elements are entering the picture. Insurance costs are expected to rise significantly in the months ahead. While property and cyber price increases are making the headlines, all lines will be impacted as the cost of claims resolution is increasing dramatically.

It’s the subject of a separate commentary to discuss ways to anticipate and manage these cost increases. Again, your broker is the key business partner in presenting you with strategies for transferring and/or retaining risk in a prudent and economical way. Sureties will want to be satisfied that the coverages in your insurance program are adequate and ‘gap free’, that deductibles, retentions, co-insurance provisions are easily funded, and the basis by which premium increases can be absorbed within your expected profit margins.

Little if any of this matters if a contractor isn’t paid for the work. On private work, sureties will be diligent to confirm funding sources and timely receipt of payment. It is important to communicate the extent to which you have done this, including reviews of loan agreements, payment for materials, confirmation that funds for the project are escrowed, and other practices to reduce your exposure to the credit risk of your owner.

Unexplained slow receivables or uncollectible underbillings may impact the capacity your surety is prepared to extend. Emphasize the extent of your firm’s revolver bank facilities to assure your surety you maintain the ability to fund liquidity needs in the short-term, if needed.

Contractors are currently confronting an increasingly unsettled and uncertain business environment. So is the surety industry. Both see increased risk ahead. For construction firms, and their brokers, who have built trust with their sureties through candid communication and data driven decision making – that risk presents opportunity.

Leave a Reply